Authors/ Yi-Meng Chao, Senior Assistant Researcher, RSPRC.

Ling-Ru Hsu, Senior Assistant Researcher, RSPRC.

Fang-Ying Lin, Project Specialist, RSPRC.

National Taiwan University's Risk Society and Policy Research Center (RSPRC) has been monitoring Taiwan's top 10 greenhouse gas-emitting companies since 2017. The center published the first edition of the "Corporate Climate Action Tracker" report in 2019 to identify Taiwan's leading industries and corporations by their greenhouse gas emissions. The 2024 edition, the sixth in the series, analyzes the latest data on greenhouse gas emissions from major carbon emitters who are required to report and register their emissions. The report notes an increase in the number of major carbon emitters from 289 in 2021 to 550 in 2022 and examines the emissions volumes and key industries involved, as well as the top 30 greenhouse gas emitters.

This report also evaluates the companies' assessment and response to climate-related risks and opportunities based on the disclosures of climate-related information made by the top 30 emitters across four key areas: governance, strategy, risk management, and metrics and targets. It also provides additional insight into the quantification of climate-related financial impacts, internal carbon pricing, supply chain reduction targets, and the climate risk and opportunity matrix. Finally, as part of the annual corporate climate action report, the document updates the proportion of Taiwan's total emissions accounted for by the top 10 and top 30 greenhouse gas-emitting companies in 2021, and it examines the key sectors, industries, and companies responsible for these emissions in Taiwan.

The Number of Major Carbon Emitters and Greenhouse Gas Emissions in Taiwan in 2022

• In August 2022, the Environmental Protection Administration (now the Ministry of Environment) announced a revision to the "First Batch of Emission Sources Required to Register Greenhouse Gas Emissions," adding a second batch of emission sources to be registered. In this revision, indirect emissions from electricity use were added to the scope and manufacturing facilities with combined direct and indirect greenhouse gas emissions exceeding 25,000 metric tons of carbon dioxide equivalent (CO₂e) were required to register. This resulted in the number of major carbon emitters (often referred to as "major carbon emitters") increasing from 289 entities in 2021 to 550 in 2022. However, despite the significant increase in the number of reporting entities, the total emissions from these major carbon emitters in 2022 were 223.244 million metric tons of CO₂, a decrease from 233.873 million metric tons in 2021. The emissions from these major carbon emitters represented 78.07% of Taiwan's total emissions of 285.967 million metric tons of CO₂e in 2022, showing little change from the 78.69% recorded in 2021 (Ministry of Environment, Climate Change Administration, 2024b). Detailed data on 2021 can be found in the 2023 Corporate Climate Action Report (Zhao Yimeng, Xu Lingru 2023).

• Among the major carbon emitters, the power and gas supply industry had the highest direct emissions, accounting for 57.10% of the total emissions. This was followed by the chemical materials and fertilizer manufacturing industry, which contributed 13.48%, and the basic metals manufacturing industry, which accounted for 12.88% (Figure 1). In terms of numbers, the electronic components manufacturing industry had the highest number of reporting entities, with 211 entities, or nearly 40% of the major carbon emitters, an increase of 116 entities from the previous year. In the chemical materials and fertilizer manufacturing industry, there were 100 entities, 53 more than the previous year. Additionally, some manufacturing sectors, such as computers, electronic products and optical products, electrical equipment and appliances manufacturing, and automobiles and parts manufacturing, appeared for the first time on the list of major carbon emitters owing to the inclusion of indirect emissions resulting from electricity use (Figure 2).[1]

Figure 1: Distribution of Greenhouse Gas Emissions by Industry for Major Carbon Emitters in 2022 (Figure Above 1/2)

Figure 2: Distribution of Major Carbon Emitters by Industry in 2022 (Figure Above 2/2)

Source: Ministry of Environment, Climate Change Administration (2024a)

Note: In Figure 1, service industry greenhouse gas emissions , at 0.0002% (0.0005 MtCO₂e) of the total, are included in the graph but are too small to be clearly visible; therefore, this clarification is required.

Greenhouse Gas Emissions from Major Carbon Emitters in Taiwan's Manufacturing Industry in 2022

• In 2022, Taiwan's manufacturing industry reached an export value of $475 billion as part of the global supply chain, accounting for 99.1% of its total export value, a significant contribution to Taiwan's economic development. The electronic components manufacturing industry alone accounted for $232.2 billion or 48.4% of the total exports (Ministry of Finance, 2024). Taiwan's manufacturing sector, however, is also the most significant source of greenhouse gas emissions, both through the combustion of fossil fuels and through the use of electricity. In 2022, the manufacturing sector emitted a total of 146.894 million metric tons of CO₂ equivalent (MtCO₂e), representing 51.37% of Taiwan's total emission of 285.967 MtCO₂e, making it a crucial sector for achieving Taiwan's net-zero emissions goal (Ministry of Environment, Climate Change Administration, 2024b). In 2022, the combined direct (Scope 1) and indirect (Scope 2) greenhouse gas emissions from major carbon emitters in Taiwan's manufacturing industry totaled 152.354 MtCO₂e,[2] an increase from 2021, primarily due to the inclusion of the second batch of emission sources in the reporting requirements, which led to a rise in Scope 2 emissions (Ministry of Environment, Climate Change Administration, 2024a). The chemical materials and fertilizer manufacturing industry led emissions with 43.820 MtCO₂e, followed by the basic metals manufacturing industry with 33.710 MtCO₂e, and the electronic components manufacturing industry with 30.256 MtCO₂e (Figure 3).

• On April 29, 2024, the Ministry of Environment announced three draft sub-laws related to carbon fees: the "Carbon Fee Collection Method," the "Designated Targets for Greenhouse Gas Reduction for Carbon Fee Collection Objects," and the "Management Measures for Autonomous Reduction Plans." The carbon fee rate, could result in the manufacturing industry being charged NT$45.7 billion if set at NT$300 per metric ton. The government will impose a carbon fee of NT$13.1 billion on the chemical materials and fertilizer manufacturing industries, followed by NT$10.1 billion on the basic metals manufacturing industry and NT$9.1 billion on the electronic components manufacturing industry.

Figure 3: Direct and Indirect Greenhouse Gas Emissions from Major Carbon Emitters in Taiwan's Manufacturing Industry in 2022

Source: Ministry of Environment, Climate Change Administration (2024a).

Taiwan's Top 30 Greenhouse Gas Emitting Companies in 2022

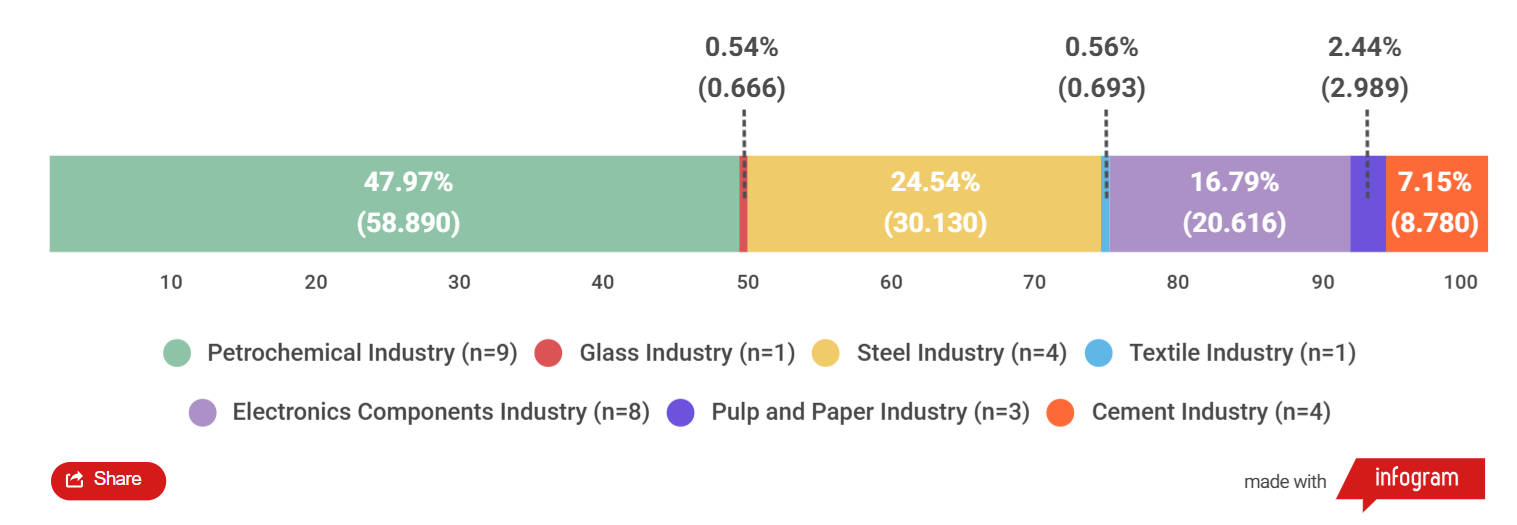

• In this report, Taiwan's top 30 greenhouse gas-emitting companies are identified by aggregating data from major carbon emitters under the same company (hereafter referred to as the "top 30 companies"), as shown in Figure 5. These top 30 companies emitted a total of 122.765 million metric tons of CO₂ equivalent (MtCO₂e), representing approximately 83.57% of Taiwan's total greenhouse gas emissions (Ministry of Environment, Climate Change Administration, 2024a; 2024b) from the manufacturing sector. Nine of these companies are located in the petrochemical industry, eight in the electronics components industry (six in the semiconductor industry and two in the display panel industry), four in the steel industry, four in the cement industry, three in the paper manufacturing industry, one in the textile industry, and one in the glass industry. Among the top 30 companies, the petrochemical industry had the highest share of emissions at 47.97%, followed by the steel industry at 24.54%, the electronic components industry at 16.79%, the cement industry at 7.15%, and the paper manufacturing industry at 2.44% (Figure 4). As compared to the 2021 list, the 2022 list of top 30 companies saw the addition of one steel company and two cement companies, while three companies were removed, one each from steel, paper manufacturing, and petrochemical industries.

• Within the top 30 companies, TSMC (Taiwan Semiconductor Manufacturing Company) had the highest Scope 2 emissions, totaling 9.249 MtCO₂e (Figure 5), primarily due to electricity consumption by emission sources required to be registered. According to TSMC's 2022 Sustainability Report, its Scope 2 emissions from Taiwan facilities reached 9.510 MtCO₂e in 2022, which was calculated using an electricity emission factor of 0.509 kgCO₂e per kWh, as announced by the Bureau of Energy in 2022 (TSMC, 2023). Therefore, TSMC's Taiwan facilities are estimated to have consumed approximately 18.7 billion kWh in 2022, accounting for approximately 6.69% of Taiwan's total electricity consumption of 279.5 billion kWh, an increase of nearly one percentage point from the previous year (5.71%). TSMC's electricity consumption also represents 30.09% of the electricity consumption in the computer, communication, and audiovisual electronics industry, which amounted to 62.1 billion kWh (Bureau of Energy, Ministry of Economic Affairs, 2024).

• It is estimated that the top three emitters would be subject to significant charges if the carbon fee is levied at NT$300 per metric ton. Formosa Petrochemical, ranked first, would be charged over NT$7 billion; China Steel, ranked second, would be charged nearly NT$6 billion; and TSMC, ranked third, would be charged over NT$3 billion (Figure 6).

• The ranking of Taiwan's top 10 greenhouse gas-emitting companies have remained relatively stable from 2015 to 2022, with only minor changes, except for the 10th position. The largest increase in greenhouse gas emissions has been shown by TSMC, which rose from the eighth to the third position in 2022 (Figure 7). In 2022, Taiwan's top 10 companies emitted a total of 99.109 MtCO₂e, accounting for 67.47% of the manufacturing sector's emissions and 34.66% of Taiwan's total emissions (Ministry of Environment, Climate Change Administration, 2024a; 2024b).

Figure 4: Distribution of Greenhouse Gas Emissions by Industry for the Top 30 Companies in 2022 (Unit:MtCO2e)

Source: Ministry of Environment, Climate Change Administration (2024a).

Figure 5: Greenhouse Gas Emissions of the Top 30 Companies in 2022 (Figure Above 1/2)

Figure 6: Carbon Fees for the Top 30 Companies in 2022 (Figure Above 2/2)

Source: Ministry of Environment, Climate Change Administration (2024a)

Note: The table calculates emissions from both Scope 1 and Scope 2 industries, excluding the power supply industry to avoid double-counting emissions from electricity consumption in Scope 2 and emissions from the power supply industry in Scope 1.

Figure 7: Taiwan's Top 10 Greenhouse Gas Emitting Companies from 2015 to 2022 (Unit:tCO2e)

Source: Ministry of Environment, Climate Change Administration (2024a)

Note 1: The data for each year were generated by interpolation in the charting system.

Note 2: The total emission data in the chart is the sum of the emissions from 12 companies that appeared in the top 10 list between 2015 and 2022.

Climate Information Disclosure by Taiwan's Top 30 Greenhouse Gas Emitting Companies in 2022

(1) Status of Climate-Related Information Disclosure (TCFD)

Next, we examined the disclosure of key aspects of governance, strategy, risk management, and metrics and targets by the top 30 companies (see Figure 8; Appendix 1). These data were obtained from sustainability reports or TCFD reports of each company or group, along with publicly available documents such as annual reports. The reporting period covered January to December 2022 (with Micron Technology's corporate sustainability report covering the period from September 3, 2021, to September 1, 2022). As the reporting boundaries were determined primarily by the company or group, which may include overseas facilities or subsidiaries, the scope of disclosed information may differ from legal requirements.

• Among the top 30 companies in 2022, 27 provided climate-related information in their sustainability reports in accordance with the TCFD's recommendations. Only one non-publicly listed steel company and two publicly listed cement companies failed to comply with this framework. In accordance with regulations, publicly listed companies will be required to disclose climate-related information beginning in 2023. Of the top 30 companies, 28 are publicly traded, with 23 listed on stock exchanges, while only two U.S. companies are not publicly traded in Taiwan.

o The Taiwan Stock Exchange revised the "Regulations Governing the Preparation of Sustainability Reports by Listed Companies" in September 2022, in response to the Financial Supervisory Commission's "Green Finance Action Plan 2.0" in August 2020, which suggested incorporating TCFD into CSR or annual reports of publicly traded companies. With the implementation of this revision, publicly listed companies must provide climate-related information in their sustainability reports starting in 2023.[3] In response to the integration of international sustainability information disclosure frameworks, the Financial Supervisory Commission issued a blueprint in August 2023 to align Taiwan with the International Financial Reporting Standards (IFRS) Sustainability Disclosure Standards. As part of this regulation, publicly traded companies in Taiwan must begin disclosing relevant sustainability information in a phased manner in their annual reports starting in the fiscal year 2026, in accordance with IFRS Sustainability Disclosure Standards. Standard S1 outlines the "General Requirements for Disclosure of Sustainability Related Financial Information," incorporating the recommendations of TCFD. IFRS Standard S2, "Climate-Related Disclosures," supplements S1 by setting additional requirements for disclosing climate-related risks and opportunities (IFRS, 2023).

• Governance: The 27 companies that have adopted the TCFD framework have all reported sustainability or climate-related issues to their boards of directors or have had these issues overseen by them. All 30 companies have established sustainability or ESG committees or working groups to address climate-related issues, such as energy conservation and carbon reduction, carbon neutrality, net-zero emissions, and carbon risk management. Furthermore, 24 companies have disclosed climate-related incentive mechanisms or compensation policies linked to sustainability performance.

• Strategy: All 27 companies that adopted the TCFD framework disclosed the financial impacts of climate-related risks and opportunities. However, among the top 30 companies, only 19 provided quantitative disclosures, often presenting data on the impact of carbon fees or increased energy costs. Nine companies provided qualitative information through narrative descriptions, and two did not provide any financial information. Twenty-five companies conducted scenario analysis based on warming scenarios provided by IPCC, IEA, and NDC.[4] However, these analyses vary in their level of detail, with some companies failing to specify the scenarios used or disclose the results.

o Regarding the "quantification of climate-related financial impacts," any company that disclosed financial impacts from both risks and opportunities was considered to have disclosed this item. Examples include monetizing the financial impact of risks or opportunities or presenting it as a percentage of revenue or changes in costs.

• Risk Management: Risk management refers to the assessment of potential impacts related to physical and transition risks associated with climate change and the development of corresponding responses. A total of 27 of the top 30 companies disclosed measures to address physical risks, such as flooding and drought, after identifying these risks. With the exception of those firms that have not implemented the TCFD framework, all 27 companies identified policy and regulatory risks as key transition risks, with carbon pricing being one of the most significant. Fourteen companies had already implemented internal carbon pricing in 2022 to address the risks posed by carbon pricing and other transition risks. Another seven were in the planning or development stages. Detailed information regarding the climate risks and opportunities identified by these companies can be found in the following section on the "Climate-Related Risk and Opportunity Matrix."

o In terms of internal carbon pricing, any company that stated that it had implemented an internal carbon price or had integrated carbon costs into its accounting process and could explain its design and mechanism has been considered to have implemented internal carbon pricing. This applies to 14 companies. We categorized companies that mentioned internal carbon pricing as being planned, in development, or as a future goal as "in planning," and we also noted the expected implementation date; this applies to seven companies. Among the remaining nine companies, none disclosed whether internal carbon pricing had been implemented or was in the process of being implemented.

o Carbon pricing can be categorized into two types. The first is a "shadow price," which is used to assess or evaluate performance but does not involve the actual collection of funds. The second is "internal tax/fee," in which carbon prices are based on the greenhouse gas emissions of internal business units, activities, or product lines, and revenue is used to facilitate low-carbon investments or to encourage emissions reductions within the organization (TCFD, 2021). The TCFD recommends internal carbon pricing as one of the tools for managing climate risks and improving disclosure. By valuing greenhouse gas emissions associated with assets, investments, and business models, organizations are able to assess actual and potential impacts and adjust strategies as necessary to remain competitive. Organizations experiencing significant physical or transition risks, or those not yet affected by external carbon pricing, may find this tool particularly useful. Internal carbon pricing disclosures can also improve transparency and align with publicly disclosed climate scenarios (Navigant, The Generation Foundation, CDP, 2019; TCFD, 2021).

• Metrics and Targets: All 30 companies disclosed their Scope 1 and Scope 2 greenhouse gas emissions, and 25 of them began disclosing their Scope 3 emissions in 2011.[5] Additionally, 25 companies disclosed third-party verification statements in accordance with ISO 14064-1 (including some companies that may not have completed verification at the time of report publication; certain verification scopes may not have included Scope 3). Only five non-publicly listed companies did not disclose their verification status in their reports or annual reports.[6] Additionally, 26 companies have disclosed their phased greenhouse gas emission reduction targets, as well as their goals for carbon neutrality or net-zero emissions by the year 2050. Regarding supply chain carbon management, only five companies disclosed supply chain reduction targets. The Science-Based Targets (SBT) initiative's official website indicates that eight of the top 30 companies have had their SBT targets verified, with reduction targets covering Scope 1 and Scope 2 emissions and six of these covering Scope 3 emissions as well. An additional two companies have committed to SBT targets but have not yet had their targets reviewed and approved.

o For the "supply chain reduction targets," any company that explicitly disclosed its greenhouse gas reduction targets for suppliers in public documents was considered to have disclosed them, including setting phased reduction percentages for suppliers over the short, medium, or long term. Only five of the 30 companies disclosed these targets, four of which were in the electronics industry. This reflects the significant pressure faced by the electronics industry to reduce carbon emissions as part of the global supply chain. In addition, some organizations have begun incorporating greenhouse gas inventories and reduction requirements into their supplier codes of conduct or incorporating climate-related indicators into supplier evaluations and audits. Furthermore, only three out of the six companies with SBT targets covering Scope 3 emissions have publicly disclosed their supply chain reduction targets. Even though Scope 3 presents challenges in terms of data collection, methodology, boundary definition, and organizational management, its importance as a risk indicator is growing. Thus, international governments, investors, advocacy groups, and others are placing greater emphasis on Scope 3, prompting companies to improve their disclosure and management of it (TCFD, 2021).

Figure 8: Climate-Related Information Disclosure by Taiwan's Top 30 Greenhouse Gas Emitting Companies in 2022

Source: Data were sourced from the 2022 sustainability reports or annual reports of each company, with SBT data compiled based on information downloaded from the SBT website on June 19, 2024. The Industrial Climate Risk Team at the Risk Society and Policy Research Center (RSPRC), National Taiwan University, conducted the review, and the author compiled the report.

(2) Climate-Related Risks and Opportunities Matrix

• This section aims to compile the climate-related risk and opportunity matrices disclosed in the sustainability reports of the top 30 companies for 2022. Using the X-axis to plot the likelihood of occurrence and the Y-axis to plot the financial impact, the matrix summarizes and visualizes the climate-related risks and opportunities identified by these companies. This summary does not include matrices based on the severity of risk or time of occurrence. Circle sizes in the matrix indicate the number of companies that identified the same risk or opportunity.

• The majority of companies identify carbon pricing policies and regulations as transition risks with a high likelihood of occurrence and a significant financial impact. In categorizing risks, policy and regulatory risks are considered to be more likely to occur, while market risks have a greater financial impact. Reputational risks are perceived as having a lower probability of occurrence and a smaller impact (Figure 9). Physical risks are generally considered less likely to occur than transition risks by companies. Long-term risks such as changes in rainfall patterns and climate models are considered the most likely to occur, significantly higher than other long-term risks. Immediate risks, such as typhoons, floods, and other extreme weather events, are the most frequently identified physical risks by companies (Figure 10). Finally, in terms of opportunities, the development and expansion of low-carbon products and services are the most frequently identified climate opportunities by companies. The use of low-carbon energy is viewed as an opportunity with both a high probability of occurrence and a significant financial impact (Figure 11). It is important to note that companies see renewable energy as both a risk and an opportunity.

Figure 9: Climate-Related Transition Risk Matrix for the Top 30 Companies (Figure Above 1/3)

Figure 10: Climate-Related Physical Risk Matrix for the Top 30 Companies (Figure Above 2/3)

Figure 11: Climate-Related Opportunity Matrix for the Top 30 Companies (Figure Above 3/3)

Source: See Appendix 1

Note: The size of the circles represents the number of items disclosed by the analyzed companies, not the number of companies.

Taiwan's Greenhouse Gas Emissions in 2021

• Taiwan's total greenhouse gas emissions in 2021 were 297.201 MtCO₂e. After excluding carbon sinks of 21.850 MtCO₂e, the net emissions were 275.350 MtCO₂e (Ministry of Environment, Climate Change Administration, 2024b). When electricity consumption was allocated from the energy sector to other sectors, the manufacturing sector emerged as the largest emitter in 2021, with emissions totaling 157.314 MtCO₂e, which represented 52.93% of Taiwan's total greenhouse gas emissions (Figure 12).

• In 2021, the 289 major carbon emitters in Taiwan collectively emitted 233.873 MtCO₂e. Excluding the power supply industry, the top 30 greenhouse gas-emitting companies accounted for a combined 132.292 MtCO₂e, approximately 84.09% of the emissions from the manufacturing sector (Figure 12) and 44.51% of Taiwan's total emissions. The top 10 emitting companies alone accounted for 67.89% of the manufacturing sector's emissions (Figure 13) and 35.93% of the nation's total emissions. Together, the top three emitters—Formosa Petrochemical, China Steel, and TSMC—were responsible for 37.59% of the manufacturing sector's emissions and 19.90% of Taiwan's total emissions.

• Among the top 10 emitting companies in 2021, the Formosa Plastics Group dominated with four companies: Formosa Petrochemical, Formosa Chemical and Fibre Corporation, Formosa Plastics, and Nan Ya Plastics, accounting for approximately 31.22% of the manufacturing sector's emissions (Figure 13) and 16.53% of Taiwan's total emissions.

Figure 12: Distribution of Greenhouse Gas Emissions in the Manufacturing Sector by the Top 30 Industries in 2021 (Figure Above 1/2)

Figure 13: Distribution of Greenhouse Gas Emissions in the Manufacturing Sector by the Top 10 Companies in 2021 (Figure Above 2/2)

Source: Ministry of Environment, Climate Change Administration (2024a; 2024b)

Note: The "n" value in Figure 12 represents the number of companies in each industry among the top 30.

Conclusion

In summary, the review of Taiwan's major carbon emitters in 2022 shows that the revision of relevant regulations, which included indirect emissions standards, has led to an increase in the number of manufacturing companies required to disclose emissions due to their use of electricity (Scope 2). Carbon fees will be imposed on these companies in the future. Taiwan's manufacturing sector plays an important role in economic development and must also bear the significant responsibility of reducing carbon emissions. Over NT$40 billion in carbon fees are collected each year, which raises important questions about how these funds will be allocated by the government. Further research is required to determine whether the funds will assist key emissions-heavy industries, such as petrochemicals and steel, to reduce their carbon footprint while also ensuring a just transition and preventing green inflation. Conversely, as for climate-related information disclosure, Taiwan's top 30 greenhouse gas-emitting companies disclosed more climate-related information in 2022 than the average Taiwanese company (refer to previous corporate TCFD surveys conducted by the Risk Society and Policy Research Center, National Taiwan University). In comparison to the 2021 review of the top 30 TCFD disclosures, some progress has been made in areas such as climate-related incentive mechanisms, internal carbon pricing, and setting SBTs. However, most companies have not made significant progress in quantifying climate-related financial impacts and conducting scenario analysis, demonstrating the challenges they face. The top 30 companies account for more than 40% of Taiwan's total emissions. These companies face greater pressure to reduce emissions and higher transition risks than the average company. Annual reports will be required to include dedicated sustainability sections in the future. Disclosure of climate-related information will not only serve as a response to regulatory requirements and stakeholder expectations but will also serve as a tool to assist companies in assessing their own climate resilience. Regulations such as these will improve comparability and prevent greenwashing in corporate sustainability disclosures, guiding market capital toward sustainable finance objectives. For Taiwan's industries to be competitive in the net-zero transition, early adopters are expected to take on leadership roles as more companies require climate and sustainability-related knowledge and experience.

Appendix 1: TCFD Disclosure Status of Taiwan's Top 30 Greenhouse Gas Emitting Companies in 2022

Special Thanks

Illustrations: Huang Kaiwen, Wang Chujun, Chen Tzuan and Center Assistants

Participation in the Sustainability Report Review: Wu Shuxuan, Ni Yuchen, Zang Jiemin, and Shen Bohuai, Center Assistants

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

※The aforementioned may not be copied for commercial use without the center's consent, thank you.※

Notes:

[1] According to the Environmental Protection Administration’s Guidelines for “Greenhouse Gas Emission Inventories,” direct greenhouse gas emissions (Scope 1) refer to emissions directly released from processes or facilities. Energy indirect greenhouse gas emissions (Scope 2) refer to indirect emissions resulting from the use of electricity or steam.

[2] The total emissions data for Scope 1 and Scope 2 of major carbon emitters in the manufacturing sector slightly exceed Taiwan’s manufacturing sector greenhouse gas emissions. This discrepancy may be due to inconsistencies in inventory and calculation methodologies. However, the National Greenhouse Gas Emissions Inventory does not provide detailed explanations regarding the definitions and calculation methods for the manufacturing sector, which requires further clarification.

[3] While non-publicly listed companies are not required to disclose climate-related information, the Financial Supervisory Commission’s “Regulations Governing Information to be Published in Annual Reports of Public Companies” and “Regulations Governing Information to be Published in Public Offering and Issuance Prospectuses by Issuing Companies” mandate that they explain the “implementation of sustainability practices and the differences from, and reasons for, the sustainability practice codes of publicly listed companies,” with the implementation of sustainability practices including climate-related information.

[4] IPCC, IEA, and NDC refer to the Intergovernmental Panel on Climate Change, the International Energy Agency, and Nationally Determined Contributions, respectively. In addition to referring to scenarios or reduction targets published by these organizations, companies analyze physical and transition risks under different climate scenarios. They may also use climate scenario projections provided by the Taiwan Climate Change Projection Information and Adaptation Knowledge Platform (TCCIP), which simulates IPCC scenarios to offer more detailed climate scenario estimates for Taiwan.

[5] The Environmental Protection Administration has provided guidelines for greenhouse gas emission inventories. Other indirect greenhouse gas emissions (Scope 3) are those resulting from business activities that are not owned or controlled by the business. These include emissions caused by leased assets, outsourced activities, employee commuting, business travel, and upstream and downstream transportation and distribution.

[6] By implementing greenhouse gas inventory operations in accordance with the Guidelines for Greenhouse Gas Emission Inventories (2024 Edition) issued by the Ministry of Environment, companies can identify emission hotspots and develop reduction strategies. A list of the top 30 greenhouse gas-emitting companies is provided in this document based on information obtained from sources designated by the Ministry of Environment for registering and verifying greenhouse gas emissions. To upload their data, these companies must undergo verification by an authorized institution and obtain a reasonable assurance level. There are, however, some non-publicly listed companies among the top 30 that have not publicly disclosed their status as verified.